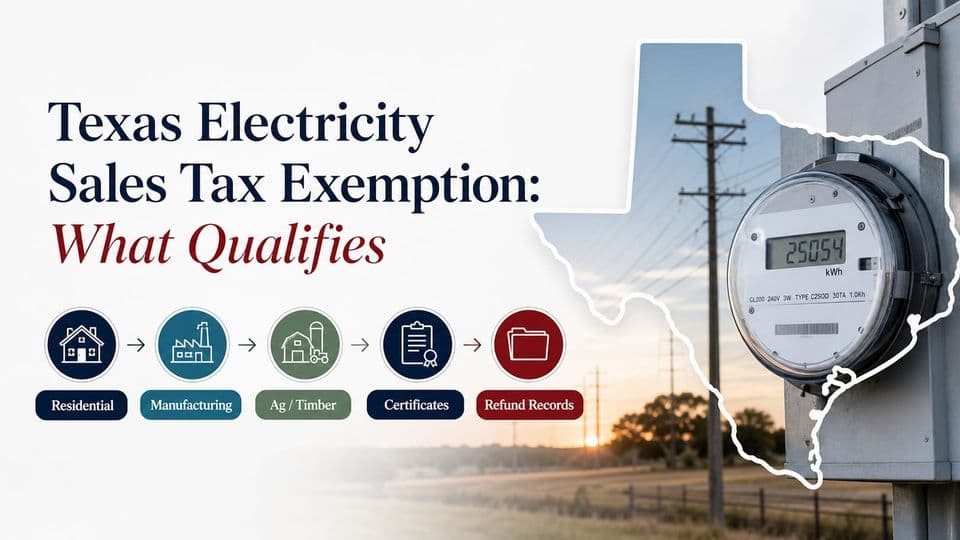

Texas Electricity Sales Tax Exemption: What Qualifies

Texas electricity tax exemptions depend on how the power is used, which official rule applies, and whether the customer has the right certificate, study, or refund support.

Key Takeaways

- 1Residential use of natural gas and electricity is exempt from most local sales and use taxes in Texas, but some local exceptions can apply.

- 2For manufacturing, Texas Comptroller guidance says gas and electricity used to power exempt manufacturing equipment are subject to a predominant use study.

- 3For agricultural and timber operations, the Comptroller lists electricity and natural gas among exempt purchases that require the proper certificate and a current Ag/Timber Number.

- 4Refund questions should be checked against the Texas Comptroller's written-claim, limitation-period, and supporting-document requirements.

Texas Electricity Sales Tax Exemption: What Qualifies

If you run a manufacturing plant, operate a farm, or simply pay a residential electric bill in Texas, you might wonder whether sales tax on electricity applies to your account.

The short answer is that Texas treats electricity sales tax differently depending on how the power is used, where the customer is located, and which official exemption rule applies. This article explains the key paths and what documentation may be required, with all guidance anchored to Texas Comptroller sources.

The Short Answer on Texas Electricity Sales Tax

Texas has a state sales and use tax, and local taxing jurisdictions can add their own portion on top of that general rate. But electricity tax treatment is not the same as taxing most retail goods.

Whether you pay sales tax on a given electric bill depends on who you are, what the electricity powers, and where the service address sits.

For residential customers, the Texas Comptroller says residential use of natural gas and electricity is exempt from most local sales and use taxes. However, certain municipalities and certain special purpose districts tied to those municipalities can impose local tax on those purchases. So a household in one Texas town may see a local tax on its electric bill while a household in a neighboring town may not.

For business, agricultural, and manufacturing accounts, the rules shift. The question is not simply whether the customer is a business but what the electricity does. The official exemption categories that are supported by Texas Comptroller guidance include manufacturing uses involving exempt equipment and qualifying agricultural or timber operations. Each path has its own certificate and documentation requirements.

This article covers the main exemption scenarios, the forms that may be involved, how refunds work, and what records to keep. It is educational background, not legal or tax advice for a specific account.

Residential Electricity and Local Sales Tax

The Texas Comptroller's utility-specific guidance states that residential use of natural gas and electricity is exempt from most local sales and use taxes. That is welcome news for many Texas households. But the exemption is not absolute.

Certain municipalities and certain special purpose districts that are tied to those municipalities can impose local sales and use tax on residential gas and electricity. That means your neighbor in the next city over might see a different tax line on their bill than you do, even if both of you buy from the same retail electricity provider.

The key takeaway for residential customers is that most local taxes do not apply to home electricity use, but the rule comes with geographic exceptions. If your bill shows a local sales tax charge and you live in a municipality that the Comptroller lists as an exception, that charge is likely valid. If you believe the charge is in error, the correct next step is to review the Comptroller's utility tax page and contact the seller.

Business Uses That May Support an Exemption

Business electricity accounts do not automatically qualify for a sales tax exemption just because the account is commercial.

The Texas Comptroller's manufacturing exemption publication provides the clearest official path: gas and electricity used to power exempt manufacturing equipment can qualify, but the equipment must be part of a listed manufacturing activity.

The same publication lists contractors, repair providers, telecommunications service providers, and data processors as examples that do not qualify for the manufacturing exemption.

That tells you the rule is about use, not business category. A machine shop that uses electricity to run a CNC mill has a different case than an office building that uses electricity for lighting and computers.

If your business is not a manufacturer, do not assume no exemption exists. Agricultural and timber operations have a separate path covered later in this article. But for general commercial or service businesses, the official guidance does not broadly exempt all electricity purchases. Each claim depends on the specific use and the right supporting documentation.

Manufacturing Equipment and Predominant Use Studies

The Texas Comptroller's manufacturing publication says that gas and electricity used to power exempt manufacturing equipment are subject to a predominant use study. That phrase sounds technical, and it is. A predominant use study is documentation that connects a facility's utility consumption to specific qualifying equipment.

A predominant use study helps demonstrate that the electricity or natural gas you are claiming as exempt was actually used to power equipment that qualifies under the manufacturing exemption rules. The study examines total utility use and identifies what portion went to exempt equipment versus other building loads such as lighting, HVAC, or office power.

The study applies when the utility use is for powering exempt manufacturing equipment. It does not say that all electricity at a manufacturing site is automatically exempt. Common areas, break rooms, and administrative offices would likely fall outside the exemption scope.

At the time of this writing, the official Texas Comptroller guidance does not specify a minimum usage percentage or require a particular professional credential for someone preparing the study. Because those details may change or be clarified in Texas Administrative Code or updated Comptroller publications.

Agricultural and Timber Electricity Use

Agricultural and timber operations have a separate exemption path that is supported by the Texas Comptroller's ag/timber page. That page lists electricity and natural gas used in agricultural or timber operations among the exempt purchases a qualified producer can make without paying sales tax.

But note an important distinction: agricultural and timber producers are not exempt entities. That means not every purchase they make is automatically tax-free. A farmer buying electricity to run irrigation pumps for a crop qualifies if the proper documentation is in place. The same farmer buying electricity for the home office on the property may not.

To claim the exemption, the buyer must provide the energy retailer with a properly completed agricultural or timber exemption certificate that includes a current Ag/Timber Number issued by the Comptroller's office. The number has an expiration date, so checking that date before submitting the certificate is necessary. The Comptroller's ag/timber page is the right place to verify current requirements.

Certificates a Seller or Provider May Ask For

If you qualify for an exemption under manufacturing or agricultural rules, the next step is providing the right certificate to your electricity provider or vendor. The form you need depends on the exemption type.

For qualifying manufacturers, the Texas Comptroller's manufacturing publication says you can give a properly completed Form 01-339, the Texas Sales and Use Tax Exemption Certificate, to your vendor instead of paying tax on qualifying items.

That form covers manufacturing equipment, materials, and supplies, including the electricity that powers exempt equipment.

For agricultural and timber purchases, the certificate path is different. The buyer must give the retailer a properly completed agricultural or timber exemption certificate that includes a current Ag/Timber Number. This certificate is not the same as Form 01-339, and the two paths should not be confused.

The certificate path depends on the exemption type and the seller or vendor processing the purchase. A single facility may need different certificates for different types of exempt purchases. Always start with the Comptroller's official guidance for the specific exemption you are trying to claim.

Refund Requests for Tax Already Paid

If you paid sales tax on electricity that should have been exempt, you may be able to file a refund claim with the Texas Comptroller. The official refund page provides the framework.

Refund claims must be made in writing and must identify the period for which the overpayment occurred. The claim must be submitted within the applicable limitation period, which the Comptroller generally describes as four years from the date the tax was due and payable. Exact time frames can vary, so check the current refund page for the precise limitation language.

Supporting documentation is critical. The Comptroller lists examples such as invoices, transaction dates, purchase descriptions, exemption certificates, proof of payment, and identification of the local taxing jurisdiction. When applicable, utility predominant use studies can also be part of the supporting documentation for a refund review.

One additional note: a client who does not hold a Texas sales and use tax permit may need to ask the seller (i.e. the energy provider) for a refund first or obtain an assignment of the right to refund from the seller. This step adds time to the process, so plan accordingly.

Records to Gather Before Submitting a Claim

Before you submit a refund claim or prepare an exemption certificate, gather the records that support your case. The exact list depends on the exemption path, but some common categories appear across the Comptroller's official guidance.

For any claim, you will need invoices that show the transaction dates, purchase descriptions, and the tax paid. Proof of payment is also expected, so keep bank statements or payment confirmations. If the claim involves local tax, documentation identifying the municipality or special purpose district is useful.

For a manufacturing exemption claim, records should connect the electricity use to qualifying manufacturing equipment. This is where a predominant use study fits in. The study documentation, along with a completed Form 01-339, helps show the Comptroller what portion of utility use qualifies.

For an agricultural or timber claim, the key records are the agricultural or timber exemption certificate with a current Ag/Timber Number and its expiration date. Keep a copy of the certificate you provided to the seller.

Organizing these records before filing a claim or certificate saves time and reduces the chance of a rejection due to missing information.

Cautions Before Relying on Third-Party Exemption Advice

Many websites and tax service firms offer detailed guidance on Texas electricity sales tax exemptions, including specifics about threshold percentages and who can sign a predominant use study. Some of that information may be accurate, but some may not reflect current official Texas Comptroller guidance.

The safest approach is to use the official Comptroller pages as your controlling source. The Comptroller's sales tax page, utility page, manufacturing publication, ag/timber page, and refund page are the authoritative references for any claim you make.

Electricity Sales Tax Exemption FAQs

Editorial standards

SlashPlan publishes independent guidance to help Texans compare electricity plans. Our editorial team reviews each article without advertiser influence. See our editorial guidelines and monetization disclosure.

About the author

Roi CahanaEnergy advisor helping Texans better understand their electricity options and make more confident decisions. Focused on simplifying electricity plans, explaining confusing terms, and sharing practical guidance to help readers avoid common mistakes when comparing rates, contracts, and renewals.

Ready to compare plans?

Enter your ZIP code to see electricity plans available at your address.